Mi SciELO

Servicios personalizados

Servicios personalizadosServicios Personalizados

Articulo

texto en

texto en  Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por emailIndicadores

-

Citado por SciELO

Citado por SciELO

Links relacionados

-

Similares en

SciELO

Similares en

SciELO

Compartir

Permalink

PermalinkCooperativismo y Desarrollo

versión On-line ISSN 2310-340X

Coodes vol.11 no.3 Pinar del Río sept.-dic. 2023 Epub 30-Dic-2023

Experience of good practices

Quality management and its impact on the efficiency of accounting services

1 Universidad Agraria de La Habana "Fructuoso Rodríguez Pérez". San José de las Lajas, Mayabeque, Cuba.

2 Cooperativa no Agropecuaria de Teneduría y Gestión Acerco. La Habana, Cuba.

The analysis offers a vision of the need for the quality management system as a strategic decision that can help improve performance, provide a solid basis for sustainable development initiatives, the correct realization of processes and efficiency in services. This article shows the experience of the Bookkeeping and Management Cooperative Acerco in documenting and standardizing the processes of its quality management system, the way in which some of the requirements of the standard have been approached and the advantages of this. For this purpose, the International Organization for Standardization's 9001 standard of 2015, the organization's diagnostic methods and methodological elements of popular education are articulated, with a view to implementing a quality management system that has an impact on its members, customers and suppliers, consolidating its strengths and improving its weaknesses, seeking continuous improvement.

Key words: quality management system; popular education; service processes

Introduction

Today, quality management has become a way to continuously improve the performance of an organization, which implies working to satisfy not only the end customer, but all stakeholders.

In that sense, organizations are as effective and efficient as their processes are (González Ortiz, 2016; Hernández Palma et al., 2018; Larios Gómez, 2016; Seoane González et al., 2018) so they become aware, considering how to design, improve and maintain their processes and avoid some common troubles such as: insufficient customer focus, low performance, departmental barriers, useless sub-processes due to lack of global vision, excessive inspections and redundancy (Pincay Morales & Parra Ferié, 2020).

In order to have effective processes, some good practices are: documenting processes, establishing indicators to evaluate their effectiveness, eliminating process defects and ensuring their continuous improvement. If these practices are applied in all the important processes of the company, there will be efficient, effective and adaptable processes (Otálora Luna & Gutiérrez Fernández, 2011).

To achieve these good results, organizations need to manage their activities and resources with the aim of guiding them towards achieving them (Pérez Fernández et al., 2022; Samá Muñoz & Benítez Pérez, 2019), which in turn has led to the need to adopt tools and methodologies that allow organizations to configure their management system (Castell Catalá & de la Nuez Hernández, 2021; Flores Torres et al., 2022).

In Cuba, it must be understood that the situation in which organizations are developing today is not only to understand the need for change, but also to maintain the logic between strategy, culture and processes, in addition to meeting the demands of customers, in such a way that the objectives are met, being of vital importance to develop strategies to strengthen their competitive advantages.

The Bookkeeping and Management Cooperative Acerco is one of the non-agricultural cooperatives approved in the country to provide accounting services. It is about to celebrate eight years since its creation, and its members intend to strengthen its internal management system by designing and implementing its quality management system.

They recognize that the adoption of a Quality Management System (QMS) ensures efficiency and effectiveness within the organization. Furthermore, it is a strategic decision that can help the entity improve its overall performance and provide a solid foundation for sustainable development initiatives.

Based on empirical research, it was found that, despite having defined all its processes, only 10.36% of the total processes are completely designed. In the analysis of the designed processes, it was found that not all their input elements are considered, such as: applicable legal and regulatory requirements, audit plan and strategic planning, as well as their output elements: analysis of risks and opportunities of the process, results of audits and indicators for measuring effectiveness.

Therefore, the objective of this article is to show the experience of the Bookkeeping and Management Cooperative Acerco in documenting and standardizing the processes of its quality management system.

Materials and methods

The predominant type of research is descriptive-explanatory. Descriptive statistics is used. This is based on percentage calculation, arithmetic mean, mode, construction of scales and graphs, as well as the selection, evaluation and processing of indicators.

For its development, different methods and techniques were used, such as:

Theoretical: They allow the interpretation by means of logical thought processes of the information processed statistically or not. The Historical-Logical method made it possible to study all the information about the evolution of quality and its management in the organizations.

The Analysis and Synthesis allowed to analyze and synthesize the bibliography to define the terms related to the QMS.

The Systemic approach facilitated the analysis of the interrelationships that exist between the elements of quality and thus avoids inconsistencies in its design.

Empirical: They allow gathering the necessary information and data from the practices for decision making in the research. The observation and documentary analysis were oriented to the search for relevant information, linked to the conceptual and methodological elements related to the object of the research. The questionnaires and individual interview guides were applied with the objective of obtaining information about the subject matter of the study.

For the development of the study, the type of sampling selected by the authors was non-probabilistic purposive sampling; the population was represented by seven members representing the social bodies of the cooperative under study and 80 members.

The model used to design the Quality Management System is that of the ISO 9001 standard of 2015, based on the organization's diagnostic methods and articulating methodological elements of Popular Education.

Results and discussion

Diagnosis of quality management at Acerco

The assessment of the results of each of the methods and techniques used made it possible, based on the different sources of information, to determine the strengths and weaknesses that characterize the object of study:

Strengths:

Quality and prestige recognized by customers

Innovation in services

Recognition by partners of the need for a QMS that impacts our services

Financial and material resources

The deficiencies detected in the diagnosis can be seen in the following figure.

Quality management system at Acerco

In order to determine the elements of Acerco's QMS, workshops were held and participatory techniques were applied that allowed a collective analysis to understand the current situation of the cooperative, its different components and their complexity, as well as to establish actions and activities in order to plan a strategy aimed at achieving the proposed objectives.

Scope of the quality management system

It covers the processes established in Acerco, in order to offer effective services in terms of accounting, financial and tax solutions that meet the needs and expectations of customers, partners and employees.

From the ISO 9001 standard of 2015, section 8.3 Design and Development is not applicable to the QMS, since the services provided are governed by current accounting regulations that establish the how, in addition, Acerco has defined by identified good practices the know-how for the service processes provided by the organization.

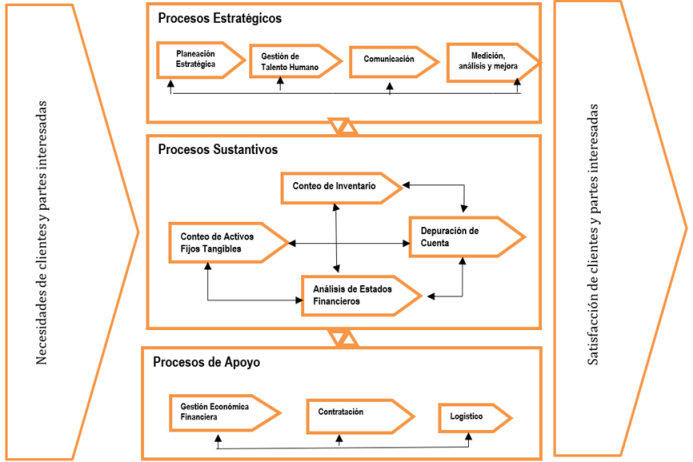

Acerco's process map was drawn up (Figure 2). Of these, four strategic, four substantive and three support processes were classified with a breakdown of their respective activities, and process sheets were drawn up for each process, describing each one to facilitate changes and planning, promoting the use of the process approach and risk-based thinking.

Source: Joint elaboration based on the workshops held

Source: Joint elaboration based on the workshops heldFigure 2 Process map of the Bookkeeping and Management Cooperative Acerco

To verify the relationships between the processes, the level of integration of the processes was established. For this purpose, a survey was made to the heads of processes to evaluate the importance and performance of the relationships between them, resulting in the matrix shown in table 1.

Table 1 Relationships between processes

| P1 | P2 | P3 | P4 | P5 | P6 | P7 | P8 | P9 | P10 | P11 | P12 | |

| P1 | I=2 D=2 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | |

| P2 | I=3 D=3 | I=2 D=3 | I=2 D=2 | I=3 D=3 | I=2 D=2 | I=2 D=2 | I=2 D=2 | I=2 D=2 | I=3 D=3 | I=3 D=3 | I=1 D=1 | |

| P3 | I=3 D=2 | I=2 D=2 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=2 D=1 | I=2 D=2 | I=1 D=1 | |

| P4 | I=3 D=3 | I=3 D=3 | I=2 D=2 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=2 D=2 | I=3 D=3 | I=2 D=2 | |

| P5 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=1 D=1 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=1 D=1 | |

| P6 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=1 D=1 | I=3 D=3 | I=1 D=1 | I=3 D=3 | I=1 D=1 | I=1 D=1 | |

| P7 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=1 D=1 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=1 D=1 | |

| P8 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=1 D=1 | I=1 D=1 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=1 D=1 | |

| P9 | I=3 D=3 | I=1 D=1 | I=2 D=2 | I=2 D=2 | I=2 D=2 | I=1 D=1 | I=1 D=1 | I=1 D=1 | I=3 D=3 | I=1 D=1 | I=3 D=3 | |

| P10 | I=3 D=3 | I=2 D=2 | I=3 D=3 | I=3 D=3 | I=2 D=2 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | |

| P11 | I=1 D=1 | I=2 D=2 | I=1 D=1 | I=2 D=2 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=3 D=3 | I=2 D=2 |

Source: Authors' elaboration

The matrix shows that there are 80 relationships of high importance, none of which is critical. Through this analysis, the level of internal integration of processes (NISDE in Spanish) in Acerco was calculated.

Internal NISDE = 1- (Internal critical ratios / Internal significant ratios)

Internal NISDE = 1- 0/80=1 There is high interrelation between processes

Acerco has decided to design, implement and maintain a QMS that is effective and efficient, with a commitment to continuous improvement and adaptation to new changes in order to achieve the goals proposed in each cycle of its management.

Quality policy at Acerco

To meet the requirements and expectations of partners, customers and employees through the provision of effective management services, integrating accounting, financial and tax solutions that achieve increased satisfaction of stakeholders, focused on the treatment of risks and opportunities, supported by an effective operation of the management system in accordance with the standards, committed to continuous improvement and compliance with applicable legal requirements. For this we have a competent staff, committed to the work and values that distinguish us.

Acerco establishes actions to address risks, responding to the risk management procedure, contained in the risk prevention plans and the opportunities contained in the improvement plans established for each of the processes in the QMS.

It also proposes its quality objectives and the actions to achieve them, deployed in all processes and levels of the cooperative.

Quality objectives at Acerco

Increase by more than 90 % the satisfaction of our customers with the quality of the services rendered

Improve the efficiency of the QMS processes to a higher level than in the previous period

The Management Body is ultimately responsible for deploying the policy, scope and objectives of quality, which are analyzed to verify compliance periodically and provides Acerco with the structures and resources necessary for the development of its activities, in order to achieve continuous improvement, sustain and increase the satisfaction of customers, partners and employees as shown in table 2.

Table 2 Responsibilities of the Administrative Body

| No | Processes | Responsibilities of the Governing Body |

|---|---|---|

| 1 | Strategic planning | It guides the cooperative towards the fulfillment of the mission, vision and strategic objectives. |

| It provides the human, financial and technological resources necessary for the processes to operate efficiently, effectively and with quality. | ||

| 2 | Human talent management | Engages staff to use their skills to achieve objectives. |

| Ensures staffing needs to keep them motivated. | ||

| 3 | Communication | Ensures proper communication with customers, partners and collaborators to promote cooperative values, the strengthening of Acerco's image and labor welfare. |

| 4 | Measurement, analysis and improvement | Ensures that quality objectives and quality policy are established, implemented and consistent with the strategic direction. |

| Ensures that the requirements of the management system are integrated into the cooperative's processes. | ||

| Ensures the integration of all system processes. | ||

| 5 | Tangible fixed asset count | Ensures the monitoring, maintenance, improvement and innovation of processes that add value for the customer. |

| 6 | Inventory count | |

| 7 | Account debugging | |

| 8 | Analysis of financial statements | |

| 9 | Economic and financial management | Maintains healthy economic growth to ensure compliance with strategic objectives. |

| 10 | Hiring | Ensures that customer requirements are correctly identified. |

| 11 | Logistics | Manages the resources necessary for the operation of the cooperative. |

Source: Authors' elaboration

In addition, it ensures the availability of resources and reviews the management system at planned periods to ensure increased customer, partner and employee satisfaction, compliance with legal and regulatory requirements, reasonable assurance in its internal control system, as well as communication channels: whether communication mechanisms were established or strengthened, including:

Design of the Acerco process sheets

For the design of the process sheets, the following steps are established:

Identify the elements that will make up the process card

Establish the measurement of the process through the definition of the indicators

Identify the risks associated with the process

Establish the activities that make up the process with their corresponding input elements and the records that are generated to represent the flowchart

Table 3 below shows the results of the work carried out for one of Acerco's QMS processes.

Table 3 Financial Statement Analysis Process Sheet

| Process: Analysis of financial statements | Code: FP-08 | ||||

|---|---|---|---|---|---|

| Objective: To ensure the financial statement analysis service provided by Acerco | Head of process: Partner in charge of control and supervision | ||||

| Scope: Financial statement analysis service provided by Acerco. | |||||

| Procedures and instructions | |||||

|

Resolution 235/2005 MFP1. Cuban Financial Reporting Standards. Resolution 386/2010 MFP. Contains NCC2 No. 1 Presentation of Financial Statements and NCC No. 3 Interim Financial Reporting. Resolution 268/2018 MFP. Internal Control Procedure No. 4. Internal control elements of the accounting subsystems. Resolution 498/2016, MFP. Contain NCC No. 5 Proformas of financial statements for business activity, special treatment budgetary units and the agricultural and non-agricultural cooperative sector. Resolution 496/2016 MFP. Specific accounting standard for budgeted activity No. 1. | |||||

| Associated records | |||||

|

Customer file (preparation or update) Diagnostic report Short, medium- and long-term projection Risk analysis Work Plan Proposed solutions Worksheet Act of Conformity | |||||

| Elements of process inputs | Suppliers | ||||

|

Strategic planning of the organization Organization Manual Internal and external procedures Information flows Procedures and organization manual Accounting manual Cost Accounting Manual Economic plan Financial statements Results of previous controls Economic and financial reports Notes to the Financial Statements |

customers customers customers customers customers customers customers customers customers customers customers customers |

||||

| Elements of process outputs | Customers | ||||

|

Diagnostic report Short, medium- and long-term projection Risk analysis Work plan Proposed solutions Worksheet Act of Conformity |

Measurement, analysis and improvement process, branch chief partners, manager and president Partners providing the service and customers Branch chief associates, administrator, president and customers Branch chief associates, administrator, president and customers Customers Partners, branch managers, administrator Branch chief associates, manager, president and customers |

||||

| Resources associated with the process | |||||

| Materials/Equipment/Other | Humans | ||||

| Laptop, calculator, sheets, Excel templates, pencil. | Acerco specialists and technicians. | ||||

| Process evaluation indicators | |||||

| Indicator | Goal | Calculation method | Frequency | Responsible | |

| % of proposed solutions that can be implemented by the partner | ≥95% | Number of solution proposals implemented / Total solution proposals *100 | Monthly | Partner in charge of the activity, branch manager partners | |

| % of customer satisfaction | ≥95% | (Total number of conformity certificates signed by the client/Total number of clients requesting the service) *100 | Quarterly | Partners, branch managers, administrator | |

| Risks associated with the process | |||||

| Risk identification | Causes of failure | Shares | Responsible | ||

| Inconsistency or errors in the primary documentation submitted |

Violation of the procedures and legislation in force by the client. Violation of internal procedures by partners and contractors. |

Establish from the contract with the client the veracity of the information requested. Perform self-preparation of current legislation and internal procedures by partners and contractors. Verify the accounting documentation before proceeding with the analysis. |

Administrator, partners, branch managers, partners and contractors | ||

| Inconsistency in the analysis of detected deviations |

Little depth in the analysis of primary documents or incomplete primary documents. |

Perform self-preparation on accounting procedures and resolutions |

Partners in charge of the business, branch manager partners | ||

| Insufficient proposals for solutions to detected deviations |

Little depth in the analysis and interpretation of accounting and financial information. |

Review the techniques and methods used Check deviations against the proposals made |

Partners | ||

| Failure to verify and correct deficiencies |

Bad service practices |

Review of the work performed, to detect deficiencies in the procedure |

Specialist partner, branch manager partners | ||

Source: Authors' elaboration

Acerco's quality management system is a strategy to increase competitiveness, based on the analysis of processes and indicators as a necessary factor to achieve the satisfaction of its stakeholders; it is the result of articulating the ISO 9001/2015 standard, with the methods of diagnosis of the organization and the methodological elements of popular education, which allows the collective construction of the system and identify, from good practices, define the interrelationships between the elements that make it up, which enhances its consolidation in terms of mastery by each member of the organization, the role it occupies from an integrative vision, with a view to continuous improvement.

REFERENCES

Castell Catalá, A., & de la Nuez Hernández, D. (2021). Diagnóstico del subsistema calidad en la Unidad Básica de Producción Cooperativa «Julián Alemán». Cooperativismo y Desarrollo, 9(2), 689-711. https://coodes.upr.edu.cu/index.php/coodes/article/view/424 [ Links ]

Flores Torres, D. A., Artola Pimentel, M. de L., & Tarifa Lozano, L. (2022). Planificación de la calidad de los procesos en el Instituto Tecnológico Superior Cordillera. Universidad y Sociedad, 14(S2), 76-83. https://rus.ucf.edu.cu/index.php/rus/article/view/2761 [ Links ]

González Ortiz, Ó. C. (2016). Sistema de gestión de calidad: Teoría y práctica bajo la norma ISO 2015. Ecoe Ediciones. https://www.ecoeediciones.mx/wp-content/uploads/2016/09/Sistemas-de-gestio%CC%81n-de-calidad-1ra-Edicio%CC%81n.pdf [ Links ]

Hernández Palma, H., Barrios Parejo, I., & Martínez Sierra, D. (2018). Gestión de la calidad: Elemento clave para el desarrollo de las organizaciones. Criterio Libre, 16(28), 169-185. https://doi.org/10.18041/1900-0642/criteriolibre.2018v16n28.2130 [ Links ]

ISO. (2015). Sistemas de gestión de la calidad-Requisitos (ISO 9001). International Organization for Standardization. https://www.iso.org/obp/ui/#iso:std:iso:9001:ed-5:v1:en [ Links ]

Larios Gómez, E. (2016). La Gestión de la Competitividad en la MIPYME Mexicana: Diagnóstico Empírico desde la Gestión del Conocimiento. Revista de Administração da Unimep, 14(2), 177-209. http://www.bibliotekevirtual.org/index.php/2013-02-07-03-02-35/2013-02-07-03-03-11/1932-rau/v14n02/20058-la-gestion-de-la-competitividad-en-la-mipyme-mexicana-diagnostico-empirico-desde-la-gestion-del-conocimiento.html [ Links ]

Otálora Luna, J. E., & Gutiérrez Fernández, E. I. (2011). Herramienta de gestión de calidad para el proceso de software, orientada a Mipymes basado en la norma ISO/IEC 15504. Revista Virtual Universidad Católica del Norte, (33), 315-327. https://revistavirtual.ucn.edu.co/index.php/RevistaUCN/article/view/20 [ Links ]

Pérez Fernández, D., Urquiola Sánchez, O., & Alpizar Fernández, R. (2022). Sistema de gestión de calidad de la Universidad de Cienfuegos. Universidad y Sociedad, 14(3), 161-169. https://rus.ucf.edu.cu/index.php/rus/article/view/2853 [ Links ]

Pincay Morales, Y. M., & Parra Ferié, C. (2020). Gestión de la calidad en el servicio al cliente de las PYMES comercializadoras. Una mirada en Ecuador. Dominio de las Ciencias, 6(3), 1118-1142. https://www.dominiodelasciencias.com/ojs/index.php/es/article/view/1341 [ Links ]

Samá Muñoz, D., & Benítez Pérez, K. (2019). Calidad directiva y su influencia en la productividad. Experiencias de la Empresa de Cemento "Mártires de Artemisa". Folletos Gerenciales, 23(3), 148-159. https://folletosgerenciales.mes.gob.cu/index.php/folletosgerenciales/article/view/211 [ Links ]

Seoane González, J. M., Jaya Escobar, A. I., & Guerra Bretaña, R. M. (2018). Proceso de transición a la norma NC-ISO 9001:2015 en la empresa mixta Suchel Camacho S.A. Revista Caribeña de Ciencias Sociales, enero. https://www.eumed.net/rev/caribe/2018/01/empresa-suchel-camachosa.html [ Links ]

Received: November 19, 2022; Accepted: December 11, 2023