My SciELO

Custom services

Custom servicesServices on Demand

Article

text in

text in  Spanish (pdf)

Spanish (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO

Related links

-

Similars in

SciELO

Similars in

SciELO

Share

Permalink

PermalinkMendive. Revista de Educación

On-line version ISSN 1815-7696

Rev. Mendive vol.22 no.1 Pinar del Río Jan.-Mar. 2024 Epub Mar 10, 2024

Original article

Quality factors in the professional accounting career at the Peruvian public university

1Universidad Nacional Mayor de San Marcos. Perú

The quality of university professional training, currently required by law, is conditioning the permanence of universities in the educational market; For this reason, the objective of this research was to carry out an analysis of the factors that allow the educational quality of the professional accounting career in the Peruvian public university. The research had a qualitative design, with an evaluative and action research approach, because the researchers are in turn members of the Quality Committees of the Faculty of Accounting Sciences. The inductive inferential method was used for the analysis and systematic review of documents linked to accreditation processes in careers of the Faculty of Accounting Sciences, taking as reference the Accreditation Model applicable in Peru. The results indicate that, despite the economic difficulties, due to State budget restrictions, the public university has implemented actions that clearly highlight academic quality. Among these factors we have: periodic review of the Graduation Profile, through the performance of academic events at the beginning of the semester that allow different interest groups to gather and collect suggestions for improving said profile; On the other hand, the implementation of tutoring programs is allowing the academic environment to improve and therefore educational achievements; in addition to the systematic linking of the management of these aspects; However, there are some gaps in reference to the accreditation model, which, in some way, tend to be opportunities for continuous improvement.

Key words: Accreditation; Quality; Government; University

Introduction

The institutional context of university professional training in the last two decades is determined by regulation as an accreditation of the quality of higher university education, which in Peru presents, especially to the public University, a challenge to university autonomy, established in the Constitution. of 1993, and explicitly stipulated in constitutional norms in the last 100 years. CONEAU, the institution originally in charge of licensing universities, had limited scope and success, and in 2015, the new University Law, with a markedly liberal and anti-state tone, prescribed new and broader powers to SUNEDU (National Superintendency of Higher University Education) and SINEACE. (National System for Evaluation, Accreditation and Certification of Educational Quality), the first, created as a maximum executive regulatory entity to decide whether a university has authorization to operate or not. SUNEDU began with the "licensing" of the Universities, a process that led to the closure of 48 universities to date (01/15/2022). To date (02/24/2023), 95 licenses have been granted.

SINEACE, for its part, in charge of accrediting the quality of university higher education, establishes the mandatory accreditation of Medicine, Education and Law careers, and Doctorate programs, being elective in all other cases.

The accreditation of quality higher education emerges as a trend in Europe, quickly spreading to the American continent. The trend towards accreditation has two primary sources: one of them is the university community itself, which makes the concept of quality assurance its own, coming from the organizational context, and assumes it as part of the process and continuous improvement approaches. But, the most important source comes from the State or government, in this case supranational, taking the case of the European Union, whose fundamental intention is to control the efficiency of public spending on education, for the purposes of social validation. In this aspect, the state is strongly driven by vast corporate sectors, from the perspective of both the efficiency of the State, budgetary austerity, and the social and political designs of their interest, which are related to a so-called in the corporate press media "university reform", underlying, contrary sensu to the University Reform of 1910 in South America, initiated in Córdova, Argentina.

Professional accounting training is the specific aspect in the chosen study population, the Faculty of Accounting Sciences of a public University, the Universidad Nacional Mayor de San Marcos. According to Mantilla-Falcón et. to the. (2018), who were based on Flores & Hidalgo (2013), considered the professional competencies of the accountant to be:

"1) Timely determination of tax obligations. 2) Formulation of General Accounting and EEFF for decision making. 3) Formulation of cost, record and control systems. 4) Societal advisory. 5) Financial Advisory. 6 "Advice on annual planning for the best management of resources and capabilities. 7) Audit and internal control. 8) Labor advice on obligations and employment contracts."

In the seven competencies in Peru, it is necessary to reinforce the sense of suitability of the accountant as he is the one who formulates and executes ethical advice (Archila and Rangel, 2021; Cruz-Pérez & Cordero-Díaz, 2022) to carry out his work. professional. Compliance with the requirements of being an expert in accounting management and not in the specific task of bookkeeper is required (Salazar-Jiménez, Álvarez-Arango, Cardona-Pérez and Legarda-López, 2019). For example, in the item referring to auditing and internal control, it is necessary to provide proactive competencies in accordance with the needs of the market (Araya 2019).

Finally, social demands are reformulated due to crises or drastic changes in the internal or external market, for which prospective and projective students are required for future accounting management.

In the area of threats to the accounting profession, training outside the requirements of the labor market is included, which requires analytical capacity, soft skills, business knowledge through incubators, and accounting competency to solve from the profession. problems in real time (Blasco, Costa & Labrador, 2023; Díaz, & Choy, 2023; Gómez, 2015). In addition, the distortion of other professions that fall within the scope of the accounting professional due to having other skills necessary in professional work (Gaibazzi, Berizzo, & Trottini, 2021; Garcia da Matta, Gonçalves, Betti, & Costa, 2021)

The regulation leading to the accreditation of the quality of Higher Education began in 2006, with the creation of the National System of Evaluation, Accreditation and Certification of educational quality (SINEACE), a technical body attached to the Ministry of Education, about to turn 20. years, the direct or indirect impact produced by the accreditation regulation would have to be established.

The accreditation processes can be promoted by regulatory mechanisms of incentives from the State, and by mechanisms of greater transparency of information on quality indicators of the Universities through the computer platform of the National Superintendency of Higher University Education.

The Universidad Nacional Mayor de San Marcos, UNMSM, is the public university with the greatest prestige nationally and internationally; It is a reference for other universities in Peru. Its prestige was earned from its founding time and strengthened throughout its institutional life. Therefore, it is important to highlight that it was not the regulatory framework of Accreditation that led UNMSM to university quality, but rather its institutional philosophy of offering academic quality for the good of Society. University Law No. 30220 indicates that the accreditation of educational quality is voluntary, and its procedures aim to improve the quality of the educational service.

Currently, SINEACE, through the accreditation process, verifies the minimum requirements that an institution or professional program must have to obtain certification of educational quality. The process initially consists of a self-assessment, followed by improvement actions that allow us to overcome the difficulties that have been observed in the self-assessment, and then undergo external evaluation based on verifiable evidence, such as documentation and verifiable aspects in situ.

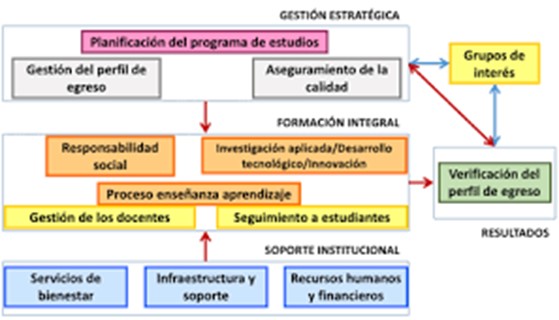

For this accreditation process, SINEACE was based on a model of four general categories, which it called dimensions: Comprehensive training, strategic management, institutional support and results. The dimensions are broken down into factors, which in turn are divided into standards, which are the minimum evaluation criteria; In total, 4 dimensions, 12 factors and 34 standards were established. (SINEACE, 2017). It is in relation to these dimensions and factors that the Quality Factors applicable to accounting training were identified for its continuous improvement.

Source: National University of the Center

Source: National University of the Center Fig. 1 - Dimensions and Factors of the SINEACE Quality Model.

This model is applicable to all university study programs; In such a way that accounting careers to achieve accreditation must comply with the 34 established standards, but in accordance with the nature of the professional career. It should also be taken into account that the compliance standards of this model are linked to each other; Thus, an implemented action can favor not only one standard, but two, three or more quality standards. For all of the above, it is the objective of this article:to carry out an analysis of the factors that allow the educational quality of the professional accounting career in the Peruvian public university.

Materials and methods

The research had a qualitative design, with an evaluative and action research approach, because the researchers are in turn members of the Quality Committees of the Faculty of Accounting Sciences. It has been used from the systematic review of the documents concerning the accreditation processes completed by the Faculty of Accounting Sciences in 3 of its courses; especially Self-Evaluation Reports, the Report of the External Evaluation Visit and the Response of the Professional Schools to the External Evaluation Visit. Thus, the reported activities have been compared with the standards indicated in the respective accreditation model. The study was carried out during the period 2023, at the aforementioned Faculty, located in the City of Lima, Peru. The units of analysis were the formal documents and reports already mentioned, coming from the external evaluation process of the accreditors SINEACE (national), CACECA, and ACBSP (international).

The data collection instruments have been Data Recording Sheets. An inductive inference analysis was applied based on the information collected, and also the panel consensus method among the research teachers, for which the same categories of the Data Model were used. SINEACE accreditation, which establishes the "gaps" between what is established in said Model that is not found in the verified facts. This is to establish and prioritize the main deficiencies that the courses of the Faculty of Accounting Sciences must overcome to improve their quality levels. The set of data collection instruments was structured, according to the dimensions, factors and standards corresponding to the SINEACE Accreditation Model, with the objective of identifying those Quality Factors (corresponding to the Model standards) that presented observations by the entity delegated for the report of that external evaluation, in accordance with the provisions of the Model. It is therefore of great interest to compare the results in the present study with those presented in other similar university training institutions.

Results

It began with the analysis of the SINEACE Accreditation Model, which is noticeably more detailed than those of other international accreditors. After this first analysis, the opinions of 3 accreditors - two foreign and one national - were reviewed. The data collection was structured according to the SINEACE Dimensions and Factors to make a more structured and expeditious analysis; a model of four general categories, or Dimensions: Comprehensive training, strategic management, institutional support and results. The dimensions are broken down into 12 factors, which, in turn, will be divided into 34 standards.

In the case of the standards of Dimension 2, Comprehensive Training, the accounting program must propose teacher selection procedures. In this Dimension, to achieve the standards that comprise it, it is important that the program implements an annual special teacher strengthening and training plan; that guarantees professional updating, which in the accounting field is of great need due to the continuous modifications of the standards linked to accounting tasks; for the benefit of students, which must include mobility through agreements with other national and international universities, to generate exchanges of experiences. The participation of teachers and students allows the internationalization of the study program.

The accreditation model presupposes the existence of a relationship between the teaching-learning processes with research, development and innovation activities, which are consistent with the provisions of Law 30220 (2014), which indicates that research constitutes a function essential and mandatory of the university, which promotes and carries it out, through the production of knowledge and development of technologies, responding to the needs of society, with special emphasis on the national reality (Art. 48).

In the case of accounting programs, research can be carried out in different economic areas; The new business mechanisms induce accounting to generate effective responses for the recognition of said economic reality, making research necessary to implement models in accordance with these changes.

In addition, research activities are encouraged in the university community through research projects by teachers and students with the support of institutional funding. We must highlight that teachers' research is considered one of their main functions (Law 30220, 2014, Art. 79); Therefore, university professors must define their lines of research and in the case of the accounting program, the research work must allow them to overcome some discussions that remain to date, to strengthen the theoretical and scientific bases of accounting and solve problems. that are generated in the different fields of action of the public accountant.

On the other hand, the University Law provides that the student must be involved in scientific research activities from the first cycles of studies, which will allow them to generate a final investigation for the purposes of obtaining the professional title. The university, for its part, must implement the regulatory framework and the necessary guidelines that facilitate the completion of the theses.

Another important activity that must be related to the study program is university social responsibility, which, according to the University Law, represents the management of the impact of the University on Society through its missionary activities, especially on development. economic, the environment and its interest groups. Accordingly, in the accounting programs, the academic activities are aimed at the specialization of their students in accounting, tax, financial, auditing, among others, disciplines of great importance for the institutional economic and financial management and development of companies and/ or public organizations.

As part of institutional support, universities have implemented support areas to achieve comprehensive training. Wellness services are implemented by universities and/or study programs, their purpose is to generate student support services, such as: the provision of health care, food, housing, mobility, sports, job opportunities, among others.

Institutional support also involves the implementation of information and communication systems that optimize enrollment, research, library, administration, financial and budget management. They must include the implementation of physical spaces and digital platforms, with information accessible to the university community.

Finally, in the results dimension, actions linked to graduates must be carried out, and with the implementation of tools so that the graduation profile can be evaluated and permanent links generated with the graduates of the study program.

Regarding the results of the information from the Response of the Preliminary Report to the external evaluators - Raising observations from the 3 professional schools of the Faculty of Accounting Sciences (UNMSM) in 2019, the data collection specifically focused to the so-called "gaps", defined as the difference between what is regulated or what is desired in accordance with the standard and what is found in reality. In accreditation models, in this case SINEACE, the "gaps" presented should be responded to with Improvement Plans, which constitute commitments of the Study Program to reduce said gaps in a time period defined by the program itself. It is also worth noting that the gaps presented are related to the specific conditions, to the nature of the programs and the University, and to the evolution of said programs.

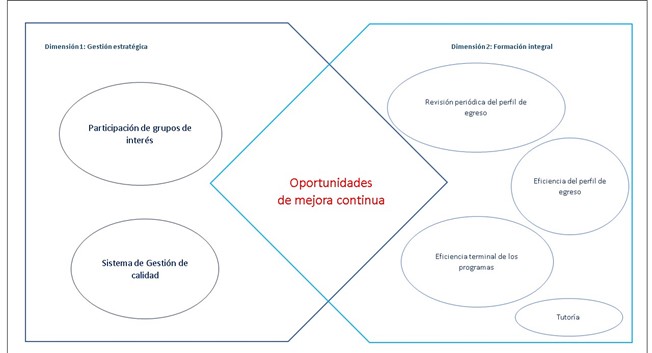

It was possible to prioritize that the most notable deficiencies or gaps correspond to the following aspects, which are the Quality Factors, named in the Accreditation Model as dimensions and factors, which were summarized in the following figure:

Fig. 2 - Opportunities for Improvement in Professional Accounting Training in a Peruvian public university, 2023.

Each opportunity for improvement detected is explained below.

Quality Management System (QMS). In this central aspect of Dimension 01 (Strategic direction), the observation of the accreditors was that there was no evidence of the existence of a QMS in order. The faculty considered at the time that the adaptation of the activities and the respective documentation to the accreditation standards constituted an incipient QMS. However, in the opinion of the accreditors, an appropriate level of systematicity and more convenient information for an authentic audit of academic quality had not yet been reached. In addition, it is clear that in any organization in which there are no truly organized management and information systems, any audit will not be able to obtain truly objective results. For this reason, the Faculty of Accounting Sciences included this item among the 14 proposed improvement plans, which allowed the respective standards to be accepted due to the conviction that it was taking the corrective measures of the case.

Terminal efficiency of programs. In this regard, related to Vocational Training (Dimension 2), the external evaluation reports showed a deficiency, to the extent that Peruvian regulations do not require an end-of-career exam that can evaluate the training of the competencies established in the study programs. A central aspect in this regard was that, due to the requirement of a graduation by thesis, required by the University Law of 2016, whose definitive implementation took place as of 2022, it shows the gaps both in relation to teaching advisors and thesis directors for the undergraduate students, which in some sense greatly exceeded the size of the faculty. For this reason, for collaboration and this terminal efficiency of the programs, it was decided to reinforce the graduation process by thesis, among other measures, by the formulation of a Thesis Development Guide, as presented by many universities in the country, which It should serve both students and thesis supervisors, for more expeditious work.

Checking the efficiency of the exit profile. Aspect related to both Vocational Training (Dimension 2) and Evaluation and Monitoring (Dimension 4). The external evaluation reports related to accreditation showed the impossibility of timely establishing a system for evaluating the competencies of the graduates over time, due to the delay in the establishment of a Monitoring and Linkage System with the Graduate, regulated by the institution itself. University. For this reason, the Office of Academic Quality and Accreditation, OCAA, included as a prioritized improvement plan to meet the accreditation requirements in the future the establishment of a Graduate Liaison and Monitoring Committee or Unit.

Tutorships. This aspect linked to the Support Systems (Dimension 3), related to the support of students with academic problems, personal problems and students with special academic needs, presented, according to the reports of the accreditors, a relative delay, which at the time should have be completed by the Tutoring Office, belonging to the Student Guidance and Welfare Unit. The logic of this standard metaphorically corresponds to "zero defects." The opportunity of the pandemic had the effect of stagnating the operation of this office due to non-presence, which is why this aspect was also included as one of the 6 improvement plans, of the 14 established at the time, to be prioritized by the faculty.

Participation of interest groups. This item is related to both professional training (Dimension 02) and Strategic Direction (Dimension 01). In this regard, the relationship with Interest Groups, a new idea brought by Quality Accreditation, and which in itself was not part of the culture of a public University, whose patron is the State, was for this reason complicated; to such an extent that the formation of the Consultative Committees of Interest Groups, or the inclusion of representatives of the Interest Groups to the Quality Committees was always fraught with difficulties. For this reason, the group of teachers who collaborate with the Quality Committees of each career, together with the OCAA, established the need to regulate this relationship with interest groups, which is expressed both in the direction of the careers and in the definition of the graduation profile, through precise directives, which had to have a normative perspective, but which also had to be part of the culture of the faculty. All of which is part of a prioritized improvement plan.

Periodic review of the graduation profile. In this regard, entirely related to Dimension 2, Vocational Training, on the need for the complete formulation of the curriculum or Study Plan, the weight of the history of a faculty that began managing a single professional career, that of accounting, was felt. . In the process of creating new professional careers in years 2 and up to 3, such as Audit, Tax Management and later Public Sector Budget, it was required that the formulation of the curricular plan be carried out individually by each professional school, which was very difficult to implement. In this sense, historically the Faculty of Accounting Sciences established a commission for curricular evaluation and academic coordination, which brings together the directors of the professional schools and the director of the Academic Department and the head of the OCAA. However, for the external evaluation, and according to the criteria of the evaluators, in accordance with the evaluation standards; Not all the requirements for adequate curriculum review and formulation were met. Using another metaphor, we could say that the curricular design corresponds to the engineering design of the product if it were an industrial company, which is why it is an aspect that requires maximum care and attention. Therefore, this aspect of strengthening the commission of the curricular evaluation and academic coordination unit was considered as part of the improvement plans.

These aspects of improvement are multi-connected; That is, they relate to each other in multiple ways, forming a system, whose elements support each other. It is of great interest to compare the results in the present study with those presented in other similar university training institutions, and with those that should result according to the theoretical approach.

Discussion

The line of research on university academic quality and accreditation has been worked on more frequently in the last decade, as it has become one of the concerns of university organizations to maintain the prestige achieved throughout institutional life. Thus, one of the coincidences with other research is to consider that the culture of educational quality is present in universities and from its dissemination, it has generated favorable changes with the characteristic of lasting over time (Sevillano, 2017).

With respect to the results obtained and detailed in the previous sheets, Díaz (2015), as part of his conclusions, indicates that university educational quality is manifested through declared purposes, which involves internalizing quality in all university processes to obtain accreditation, and also that, since education is a priority in society, it must be treated as such and be part of State policy.

On the other hand, Fleet et al., (2014) in their conclusions point out that university accreditation as a figure of quality generates a loss of legitimacy due to social and political interests; Therefore, it is necessary to revitalize specific factors, rather than objectify them.

The SINEACE Quality Model is completely consistent with modern pedagogical, scientific and management trends, focusing on 4 Dimensions: 1) Strategic direction, 2) Professional training, 3) Support Systems and 4) Evaluation and Monitoring. These dimensions force a forced modernization of the organizational structures, practices, policies, strategies and cultures of the public University, constituting in turn a "touchstone" of them. Did the public University adapt its structures, for example, to the scientific and technological development demanded by Society?

Regarding the above, Martínez et al., (2017), specify some problems that universities face in the accreditation process, which separates accreditation from its essence itself; That is, university educational organizations use accreditation as a means of advertising; Therefore, the authors consider that academic quality must encompass the relationship with society and promote the transformation of communities.

It is clearly noted that most of the gaps identified, in general, correspond fundamentally to the budgetary limitations of a public university system not prioritized by the State or by society; and by an early culture more focused on professional practice and the privileges of the teaching staff than on true service to society. Which is also reflected in the national accreditation process as a whole and the established standards themselves.

Several spokespersons for the public University expressed at different times in recent years an opinion contrary to the new University Law and a system of accreditation of academic quality, as tailor-made for business-universities, which began to abound after the 1990s, on par with the liberal reforms established then, which included the deregulation of university education. These spokespersons for the public University considered that the accreditation standards were more appropriate for business universities. In addition, many considered that the regulation of the university system was a measure to "resize" the market, removing smaller companies from the market, which still took away a lot of the market from others of larger size and financial support. In fact, many universities disparagingly classified as "chicha" did not pass the accreditation and licensing test, and were closed.

But, on the other hand, the imposition of quality standards still had a positive impact on certain university bureaucracies, which saw their power limited and were forced to fulfill their responsibility towards Society.

In this sense, although the Improvement Plans will bring the faculties, especially the Faculty of Accounting Sciences, closer to a true Quality Management System, accompanied by an Information and Communication System in order, in general, the achievement of a complete academic quality for a change in university self-awareness from its role in the creation of science and technology to serving as a monitor of the country's economic growth, and a cultural creation that enables the Nation to collaborate in this development process. And this proposal must be understood and accepted by Society and the State.

Apparently, the conditions to accredit educational quality in the country's universities are the same. However, there are factors that disadvantage public universities and put them in unequal competition with private universities; Among these factors, we have budget restrictions that are increasingly greater. However, despite the indicated difficulties, public universities have demonstrated equal and, in many cases, greater academic quality, with the limited resources they have.

In the case of accounting degrees, from the review and analysis of the different accreditation reports and the external evaluation reports of different accreditors, it is observed that it is not enough to be carried out, but rather they must be documented; which generates slight gaps with the university accreditation model; Therefore, they constitute opportunities for continuous improvement, favorable for the university community.

All of the above has allowed us to carry out an analysis distinguishing those factors of a diverse nature that influence the educational quality of the professional accounting career in the Peruvian public university.

Referencias bibliográficas

Araya Pizarro, S. C. (2019). Competencias genéricas de los estudiantes de Auditoría requeridas por las Big Four en Chile. Cuadernos De Contabilidad, 20(49), 116. https://doi.org/10.11144/Javeriana.cc20-49.cgea [ Links ]

Archila, J. & Rangel, G. (2021). Formación ética y el reto en la educación del contador público. Innovando en la U, 1-7https://repository.unilibre.edu.co/bitstream/handle/10901/24240/articulo.pdf?sequence=1 [ Links ]

Blasco Burriel, M. P., Costa Toda, A. & Labrador Barrafón, M. (2023). Competencias relevantes en contabilidad. La perspectiva de estudiantes y empleadores. Revista de Contabilidad, 26(1), 150-163. https://doi.org/10.6018/rcsar.416001 [ Links ]

Cruz-Pérez, O. A. y Cordero-Díaz, M. C. (2022). Formación ética del Contador Público en Instituciones de Educación Superior en Colombia. Reflexiones Contables (Cúcuta), 5(1). https://doi.org/10.22463/26655543.3598 [ Links ]

Díaz, O., & Choy, E. (2023). Estado de la investigación contable en Perú: Una revisión desde la academia y el gremio profesional. Cuadernos De Contabilidad , 24, 117. https://doi.org/10.11144/Javeriana.cc24.eicp [ Links ]

Flores, A. , Hidalgo, M. (2013). Elementos del estudio de la demanda social y del mercado ocupacional de la carrera profesional de contabilidad. Quipukamayoc, 21(40), 3541. https://doi.org/10.15381/quipu.v21i40.6308 [ Links ]

Gaibazzi, M. F., Berizzo, M. L., & Trottini, A. M. (2021). Demanda de competencias digitales al Contador Público. Una mirada desde la Educación Superior. SaberEs, 13(1), 7390. https://doi.org/10.35305/s.v13i1.244 [ Links ]

Gómez Montoya, J. F. (2015). El FMI, la reducción del estado y el consenso de Washington ¿una misma cosa? Papel Político, 20(1), https://www.redalyc.org/articulo.oa?id=77739761007 [ Links ]

Mantilla-Falcón, M.; Tobar-Vasco, G.H.; Arias-Pérez, M.G., y Ríos-Urrutia, G.C. (2018). Competencias del contador-auditor en el perfil de egreso. Caso Universidad Técnica de Ambato, Ecuador. Caras de Actualidad Contable, 21(37), 90-117. https://www.redalyc.org/articulo.oa?id=25755483005 [ Links ]

Martínez, J.; Tobón, S. y Romero, A. (2017). Problemáticas relacionadas con la acreditación de la calidad de la educación superior en América Latina. Innovación educativa, 17(73), http://www.scielo.org.mx/scielo.php?script=sci_arttext&pid=S1665-26732017000100079&lng=es [ Links ]

Salazar-Jiménez, E., Álvarez-Arango, L., Cardona-Pérez, J. y Legarda-López, L. (2019). Las competencias y el desempeño laboral del contador público de la Universidad de Antioquia. Contaduría Universidad de Antioquia,75, 85-113. https://doi.org/10.17533/udea.rc.n75a04 [ Links ]

Sevillano, S. (2017). El sistema de acreditación universitaria en el Perú: marco legal y experiencias recientes. Revista Educación y Derecho, 15, https://dialnet.unirioja.es/descarga/articulo/6092894.pdf [ Links ]

Received: October 16, 2023; Accepted: February 06, 2024